Why Silicon Valley Is Still the Best (and Cheapest) Place to Start a Startup

The role of network effects in creating the industry town for startups

Notes: Data from ~June 2019. San Francisco is included in “Silicon Valley” and the scope of this article is mostly focused on startups in the US. For an updated 2020 edition, click here.

Despite what many articles say, Silicon Valley is still the only place in America where startups regularly grow to become great companies.¹ It is important to understand the origins of Silicon Valley’s success because the implications have a direct impact on where a startup founder should decide to base their startup, the probability of a ‘Silicon Valley of x’ emerging in another city, and whether the Rise of the Rest will ever happen.

It’s easy when reading these articles for Silicon Valley’s dominance to be lost among the noise because the authors are searching for ways to make their argument that Silicon Valley is on the decline. They will focus on ‘soaring’ rent, infrastructure, state or city politics, the homeless population, and more.

The one variable they ignore or deliberately obfuscate is — company success measured by valuation. This alone is what matters when evaluating whether startups have a tendancy to suceed or fail in a given city.

It could be argued that company valuation is somewhat of a lagging indicator by a few years, but typically changes in cities are relatively slow processes, to begin with. Successful startups also beget successful startups. Successful startups have those core teams of people who’ve experienced what it was like to ride on someone else’s rocketship and now want to build their own or join a new startup in a more senior position than their last. Successful startups are also full of newly wealthy founders and early employees who are eager to reinvest in new startups.

Especially for founders, deciding on where to plant your startup may be one of the most important decisions you make and there may be a compelling reason why you shouldn’t be in Silicon Valley, but I think those cases are very rare. In Paul Graham’s list of 18 Mistakes Founders Make, he lists #2 as Bad Location.

Startups prosper in some places and not others. Silicon Valley dominates, then Boston, then Seattle, Austin, Denver, and New York. After that there’s not much. Even in New York the number of startups per capita is probably a 20th of what it is in Silicon Valley.

— Paul Graham

So in which cities do startups grow to become great companies?

I looked at companies across four stages; startup, unicorn, public company, and mega-cap company. Here is what I found.

Startups

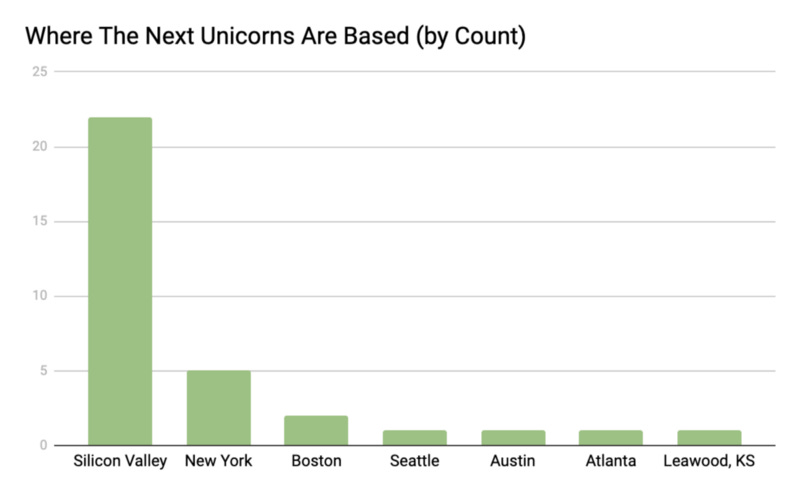

In looking at the next generation of startups, CB Insights and the New York Times put together a list of the next 50 companies around the world most likely to become unicorns, Silicon Valley accounted for 22 of them, and the next closest US city New York — accounted for 5.

Unicorns

The next phase of a successful startup’s life is to typically become a unicorn, a private company valued at over $1B. CB Insights’ latest tally of the market capitalization of global Unicorns put $323B in Silicon Valley and if you factor in the four recent IPOs that number comes to $457B. The next closest city is New York City with $114B in market cap, $47B of which is from WeWork.

I created the below chart to represent the data, I removed cities where there was only one unicorn (Magic Leap in Miami for example) as it’s not an indicator of an ecosystem, but rather one successful company. Noticeably absent are ‘emerging’ startup ecosystems that have been grabbing a lot of headlines like Boulder and Austin.

Public companies and mega-cap companies

Although increasingly delayed, going public is still the next important milestone in most startups’ growth and Silicon Valley’s 150 largest publicly traded tech companies are worth $3.5 trillion and makeup 50% of the value of the NASDAQ.² Becoming a mega-cap company with a market cap of over $100B is often the last important milestone and as of 2017, there are only 14 publicly traded tech companies in the world with market caps greater than $100 billion, 7 are in Silicon Valley.²

Additional data points on Silicon Valley’s success

A tale of two accelerators

I think the closest thing to an A/B test of America’s cities for startup success has been the tale of two accelerators. Techstars and Y Combinator started around the same time, with the same goal, have funded a similar number of companies, and generally share similar approaches, except for one important detail — location. While Techstars has started accelerators in many large American cities and some international cities, they don’t have a program in Silicon Valley. YC, on the other hand, has focused on building only one program in Silicon Valley (YC had a Boston program, but they shuttered it early on).

According to their websites’, YC has produced 19 companies with valuations or acquisitions greater than $1B and their portfolio is valued at over $100B. Techstars has produced 2 companies with valuations or acquisitions greater than $1B and a portfolio value of $17B. There is some margin for error in these numbers, but the difference is remarkable. There are of course other differences between the two accelerators, but location weighs heavily.

Silicon Valley companies win

Silicon Valley companies also tend to beat their competition. Before there was Uber, there was New York-based Taxi Magic. Before there was Airbnb, there was New Hampshire-based Couchsurfing. Before there was DoorDash, there was Chicago-based GrubHub (still being hashed out, but it’s looking like DoorDash is going to eat GrubHub’s lunch). This is a factor that often gets overlooked—Business is about winning. You don’t want to be positioned in a city that works, you want to be positioned in the best possible city to win.

Venture investment

Silicon Valley’s dominance in venture investment has only increased with time. Consistent increases in market share are a classic indicator of network-effects.

Silicon Valley’s investment per capita also significantly outperforms other cities. “Silicon Valley” i.e. San Jose, San Francisco, Oakland, and the surrounding areas account for about 3% of the US population, but accounted for 46% of venture investment in 2018.

Conventional wisdom says that Silicon Valley dominates because it has the right ingredients, but this misses a critical point

Most of the existing writing on Silicon Valley treats Silicon Valley’s rise and continued dominance as a cake-baking exercise. With the right ingredients and steps, your city can become the next Silicon Valley it seems. Y Combinator’s Paul Graham, in particular, has waxed and waned on this topic. In one case he lists out all of the different factors cities need to attract money and nerds for a city to be a startup hub, in another, he devises a plan for a city to invest a little bit in a lot of startups, and in another, he argues for why Pittsburgh could be the next startup hub only to at the end say it’s lacking one key ingredient — investors.

In reality, it is much more difficult to create a ‘Silicon Valley of x’ because you’re not just trying to replicate Silicon Valley, you’re in competition with it. He sometimes acknowledges this fact, but in general, seems much more optimistic than pessimistic on the emergence of a ‘Silicon Valley of x’ along with others such as the Rise of the Rest tour. He’s certainly right though about the dynamic between nerds and money being core to the equation, more on that later.

As the founder of a marketplace startup, I became fascinated with understanding the impact of network effects on my startup because they are core to our long-term value creation and defensibility. At the same time, I was debating whether to relocate my startup to Silicon Valley. After much research and discussion, I realized that the same phenomenon that was acting on my startup was also acting on Silicon Valley and realized the ‘cake baking’ explanations were inadequate.

Talent-driven industries, marketplaces, and monopolies

The reason Silicon Valley is so dominant is that talent-driven industries create marketplaces for talent and money in the form of an industry town with very strong network effects that create a monopoly and are nearly impossible to disrupt. Below is the progression of the creation of an industry town.

Success is highly skewed: In talent-driven industries such as film, music, and startups, many will compete, but few will win. The outcomes follow a power-law distribution. This is true of both the money and talent that must match in a marketplace for a positive outcome to occur. This has the added effect of the community of highly successful participants being relatively small.

Aggregation is key to success: To have a chance at winning, the fragmented supply and demand must aggregate in a marketplace in order to have a chance at finding the best supply and the best demand, which are both very heterogeneous and highly specialized. Matching often occurs as a result of many in-person interactions that technology has yet to replicate.

An industry town emerges: The way the industry town is chosen often comes down to being First to Market to offer initial aggregation of supply and demand, in a favorable location geographically and run reasonably well. The core requirement is the aggregation of supply and demand though, many cities around the country have favorable geography and are run reasonably well.

Network effects take over: Over time, the marketplace creates network effects where the value increases with each additional participant because there are more of them in the industry town than anywhere else. As a result, each additional film studio in Hollywood makes it more appealing for more actors to be there and each additional actor makes it more appealing for more film studios to be there. It is this aggregation of hundreds or thousands of people making these independent decisions each year that is the core of an industry town’s defensibility.

Additionally, increasing quantity also has the impact of increasing the quality of both sides of the marketplace because of increased competition. From my personal experience investors in Silicon Valley treat startups very differently than elsewhere — they respond much faster, they are more generous with their time and they agree to higher valuations.

It’s for this reason that it is actually much cheaper to start a startup in Silicon Valley than anywhere else.

Investors do not behave this way because the water in Silicon Valley naturally makes them nicer, they behave this way because the intense competition leaves them no choice. They must risk their time, higher prices (valuation), and hastier decisions or they will be left in the dust. If you’re one of only a few investors in a city, there’s minimal competition and no reason to take those risks. These network effects are powerful because they create a compounding effect which makes it illogical for an additional ambitious participant to go to any other marketplace other than the best marketplace (industry town).

As a result, for the film industry, you have Hollywood with actors (talent) and studios (money). For music, you have Nashville with musicians (talent) and labels (money). For startups, you have Silicon Valley with entrepreneurs (talent) and investors (money).

Beyond the core interaction of talent and money

In addition to becoming the best two-sided marketplace for talent and money, industry towns gradually become n-sided marketplaces for tangential talent and services, only further cementing their dominance. The increased competition amongst providers of highly specialized resources also lowers prices and creates higher quality services (startup law firms for example). You can find them elsewhere, but they are often more expensive and much less experienced. As a result, it is actually much cheaper to start a startup in Silicon Valley than anywhere else for everything beyond the core interaction of fundraising and investing.

Hiring and meeting advisors become much easier because they are everywhere and everyone seems to know everyone so you’ll find the best people in the world to help you and much faster. But yes, doing anything other than ‘the industry’ in an industry town can feel very expensive although the wealth often creates many other winners.

As a result, these talent-driven industries naturally create industry towns with the key marketplace participants and the supporting infrastructure necessary and are very difficult to disrupt because of the network effects. Elad Gil articulates this point well here and how the phenomenon also occurs in industry towns outside of the United States as well.

How Silicon Valley became the industry town for startups

Like most successful marketplaces, Silicon Valley was First to Market by creating the first marketplace for entrepreneurs (talent) and investors (money) in America. The original investors though were not venture capitalists, but rather the Department of Defense which provided funding (money) to back cutting-edge technology during the Cold War, and Stanford provided the entrepreneurs (talent). Steve Blank’s Secret History of Silicon Valley is a great source on this topic.

Many of the technologies created also had commercial applications and private venture capital started to flock along with eye-popping returns. Silicon Valley became the leader in every major technological shift and with that came the brand which has now attracted generations of talent to build great companies and the investors willing to take the risks necessary.

Silicon Valley of x

“But look at company x in y city. They were successful and didn’t move to Silicon Valley!” This is something you’ll commonly hear in discussions on this topic and yes, this is true and there are companies that have been very successful outside of Silicon Valley. You can easily rationalize why the city you’re living in is going to be the next Silicon Valley (such a great startup week!). But, when you are city agnostic and ask yourself where in America do startups succeed with regularity, there’s only one answer. Even from a cost-benefit perspective, if rent is 1.5–2x greater than other large cities, but the odds of success are 10–100x greater, the cost-benefit analysis is clear.

So are ‘Silicon Valley of x’s’ going to emerge across the United States? Is the Rise of the Rest fund going to discover hundreds of startups that have been hidden away and will get great returns? The answer is not anytime soon, and the reason is network effects.

Sources

[1] The Economist, The New York Times, and the proverbial ‘best of’ lists like this one from Inc.

[2] Reid Hoffman, Blitzscaling, Page 15.